Topics

Guests

- Daniel Brookjournalist whose work has appeared in Harper’s, the San Francisco Chronicle and the Boston Globe. He is author of The Trap: Selling Out to Stay Afloat in Winner-Take-All America. His article “Usury Country: Welcome to the Birthplace of Payday Lending” appears in the new issue of Harper’s.

- Ginna Greenspokesperson for the Center for Responsible Lending.

Lawmakers and public officials in California, Ohio, South Carolina, Missouri, Washington and other states are attempting to crack down on the controversial practice known as payday lending. Payday loans are short-term loans or cash advances secured by a post-dated check. The annual interest rate for these loans can be as high as 400 percent, ten times the highest credit card rates. Today, it’s a $40 billion industry with more than 22,000 stores. We speak with journalist Daniel Brook about his Harper’s Magazine article, “Usury Country,” and with Ginna Green of the Center for Responsible Lending. [includes rush transcript]

Related Story

Transcript

JUAN GONZALEZ: Lawmakers and public officials in California, Ohio, South Carolina, Missouri, Washington and other states are attempting to crack down on the controversial practice known as payday lending. On Wednesday, the Governor of Kentucky, Steve Beshear, signed into law a ten-year moratorium on new payday lenders in the state.

Payday loans are short-term loans or cash advances secured by a post-dated check. The annual interest rate for these loans can be as high as 400 percent, ten times the highest credit card rates. Consumers who renew their loans often end up paying more in fees than they had originally borrowed. Critics say the system is a form of a predatory lending that traps the poor in a cycle of debt.

AMY GOODMAN: In the early ’90s, there were fewer than 200 payday lending stores in the country. Today it’s a $40 billion industry with more than 22,000 stores. There are more payday lending stores than McDonald’s and Starbucks combined. As more Americans are living paycheck to paycheck, the demand for payday loans is increasing.

We’re joined now by two guests who have been following this story. Journalist Daniel Brook joins us from Philadelphia. His article “Usury Country: Welcome to the Birthplace of Payday Lending” appears in the new issue of Harper’s. He is also the author of the book The Trap: Selling Out to Stay Afloat in Winner-Take-All America.

And we’re joined by Ginna Green of the Center for Responsible Lending. The group is releasing a report today that reveals payday lenders are significantly more concentrated in African American and Latino neighborhoods in California than in white neighborhoods.

Daniel Brook, let’s begin with you in Philadelphia. A very interesting piece in Harper’s. You begin in Johnson City, Tennessee, where I’m actually headed in the next few weeks. Talk about exactly what payday loans are.

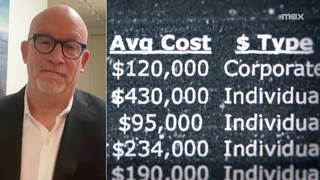

DANIEL BROOK: A payday loan is a short-term, high-interest loan. Here’s a typical transaction. Let’s say you work at a fast-food restaurant, and you’re going to get paid next Friday, but you’ve had an unexpected expense, say your car broke down, and you need money now. You would go to a payday lender. You’d write out a check for, say, $230, and they’d give you $200 in cash right then. The check, you know, would be bad, and it would be dated to your next payday. Then, when your next payday rolls around, you’re supposed to reappear at the payday lender and buy your check back in cash for the full $230 value.

Now, on the face of it, it already sounds like a high-interest loan, but it’s typically much worse than that, because the percentage of borrowers who, when their payday comes around, are able to pay it off is very small. I mean, even industry-sponsored research shows that only a quarter of borrowers are able to consistently pay off their payday loans when they come due at the end — at their first pay period. State research shows rates in the 70s or 80s or close to 90 percent of borrowers can’t pay these off. So it’s clearly a debt trap.

JUAN GONZALEZ: Now, Daniel Brook, you also profile several of the entrepreneurs who began developing these stores and then expanded them into chains — I think James Eaton, Allan Jones. How did they get to create these huge chains in such a short period of time?

DANIEL BROOK: Well, the reason the industry exploded so quickly is that it was serving a growing market. In your introduction, you said that payday loans are targeted towards the poor. And I think it depends on how we define the poor. I would say they’re targeted towards the lower middle class. I mean, anyone who takes out a payday loan has to have a bank account, which already gets rid of the unbanked, which is tens of millions of people, including 20 percent of Latinos and African Americans. So it’s people who have jobs, but they’re jobs that pay generally under $10 an hour and have inadequate benefits.

So, basically, this is a group of people that, as we know, is growing. The largest employer in the country, private employer in the country, is Wal-Mart. And we know what their wages are like. So, as this group of people who are living paycheck to paycheck — now 47 percent of Americans report living paycheck to paycheck — as this group has grown, the market for these predatory payday loans has grown, as well.

AMY GOODMAN: Ginna Green, talk about how these payday loans affect different groups of people.

GINNA GREEN: Absolutely. Thank you for having me. I wanted to also correct the introduction. You mentioned California possibly tackling payday loans this year, and it’s not clear whether or how California will do that. We’re using our report today, that you mentioned, to try and put forth the idea that California should, in fact, address payday loans.

One of the key findings of our report that’s coming out today, “Predatory Profiling: The Role of Race and Ethnicity in the Location of Payday Lenders in California,” is that in this state, payday lenders are eight times more concentrated in African American and Latino neighborhoods than in white neighborhoods. And even after we account for factors like income, education, poverty rate, we find that they’re still 2.4 times more concentrated in African American and Latino neighborhoods. I think this research has borne out what many people have thought we’ve known intuitively, that payday loans appear to really cluster in black and brown neighborhoods.

JUAN GONZALEZ: And does your report speculate on the reasons for that of the companies that do concentrate in those neighborhoods?

GINNA GREEN: You know, we’ve got the facts and the data to back up the claim, but we really can’t get to the purpose or to the intent of payday lenders. Can we say that they’re actually targeting African Americans and Latinos for a particular reason? No. And I would say that that’s a really good question for a payday lender.

What we do know is that in California, California borrowers lose $450 million a year just to pay payday loan fees. Of that amount, more than half, $247 million, comes from African American and Latino borrowers.

AMY GOODMAN: Daniel Brook, explain exactly how you take out a payday loan, the process of going into the store, and again, who started these stores and why they’ve grown into this, what, $40 billion industry.

DANIEL BROOK: Well, the process seems quite innocuous at first. I went into a Check Into Cash store. This is the company I profile, which is the first of the major national payday lending firms. And you fill out a basic two-sided information sheet with your name, the name of your landlord or mortgage holder, three people in the community who know you well, your employer and your spouse. And it takes, you know, really a matter of minutes. You write your check, and you get your cash. When this document sort of comes around to bite you is if — when and if you fall behind on payments. And at that point, all of these people start getting collection calls, as well as you, yourself, who took out the loan.

As I said, this was in Check Into Cash, which was the first of the national payday lending chains, and it was founded by a man named Allan Jones, who I had the pleasure of interviewing at his headquarters in Cleveland, Tennessee. Mr. Jones is a rather fascinating character and quite taken with his own being a fascinating character. Essentially, Cleveland, Tennessee’s culture has been hijacked by Jones. I went on Halloween, when the local townspeople make a pilgrimage to the history museum to look at the costume that Allan Jones created for his daughter’s birthday many years ago. Then they go to the block party and concert that Allan Jones created to get the townspeople off of his lawn, when he used to appear in costume as Tall Betsy, who he had named the official ghoul of Bradley County, Tennessee.

JUAN GONZALEZ: Daniel Brook, especially these chains, I would assume that they would need some investors or some capital to be able to expand rapidly and provide this cash to the working poor. Did you look into what were the financial institutions that were investing or behind these chains?

DANIEL BROOK: Yes, I did. Check Into Cash itself is a privately held company controlled by Allan Jones. But they told me, when I went to company headquarters, that they had a large line of credit from Wells Fargo Bank. Some of the other chains, including Advance America, which is the largest of the payday lending chains, are publicly traded on the stock exchange and are funded — have lines of credit from all the major banks in the United States, including Citigroup, JPMorgan, etc.

AMY GOODMAN: Daniel, you mentioned, you know, you get calls if you don’t pay back your loans, but could you go more into that? The frequency of these calls and the relationships that they develop?

DANIEL BROOK: Yeah. Well, initially, when you go into the store, they cultivate these sort of chummy customer relationships between the person behind the desk and the debtor. It’s typical, and they’re actually instructed in training to, you know, ask about the person’s family and their job and how they’re doing. Of course, these relationships get more and more strained as the person gets more and more desperate and farther and farther into debt.

JUAN GONZALEZ: I’d like to ask you, Ginna Green, in your report for the Center for Responsible Lending on the California situation, could you talk to us about what were some of the epicenters in California of this saturation of these lending institutions?

GINNA GREEN: Absolutely. As you can imagine, Los Angeles, with approximately 313 payday stores in the city, was one, and a large proportion of African Americans and Latinos was one of the epicenters of this problem. We will have interactive payday maps, as well as maps documenting this concentration, on our website later today.

What I wanted to note about what Daniel was just saying earlier, about the debt trap and how these are — the payday loans are a fundamental problem, because they trap people in cycles of debt, what — one of the reasons why our policy recommendation for payday loans is a simple 36 percent rate cap that covers all small loans is because it’s the only thing that works, and it’s the only thing that will keep — that will protect the working poor, it’s the only thing that will protect African Americans and Latinos in California. What we found is that more than half of borrowers tend to just take a payday loan because the location was right there. So that proximity and that clustering for African Americans and Latinos is really critical. Having them in communities makes people more likely to just walk in and take a loan.

AMY GOODMAN: Daniel Brook, in addition to writing your piece, “Usury Country,” in Harper’s, you’ve written a book, The Trap: Selling Out to Stay Afloat in Winner-Take-All America. And I’d like you to talk about how this, how these payday loans fit in with the bigger story, especially a story we did last week with Reverend Jesse Jackson, and that is the story of student loans.

DANIEL BROOK: Yeah. In The Trap: Selling Out to Stay Afloat in Winner-Take-All America, I look again at this rising economic inequality in the United States, this growing gap between rich and poor. The Trap focuses on a different group of people. If payday loans are for the lower middle class or working poor, we might say, The Trap is about college-educated professionals. But it argues that this increasing gap between rich and poor poses problems for this group, as well, which, of course, compared to the lower middle class is, of course, relatively well-off.

And the choice it imposes on the upper middle class is not whether or not to take out a payday loan, but whether or not to sell out, whether or not to do a job that will pay them a lot of money, but in which they don’t believe and which will both sort of hurt the country, in that they’re not doing something more service-oriented, but also make them feel like they’ve sold out. So student loans are a big part of the trap. As we’ve shifted towards a privatized system of higher education, relying more and more on debt and more and more specifically on bank-issued private debt, the debt loads of students who attend both public and private colleges, and particularly professional schools and graduate schools — and the University of California at Berkeley, which is ostensibly a public school, charges $25,000 tuition for its law school, so even students from public schools are emerging with large debt loads — end up — it ends up dictating career choice to a very disturbing extent.

I think it’s one of the things that drives a lot of the troubling trends in our society politically, including the revolving door in Washington, where people who had, say, worked in a congressman’s office on issues they believed in turn around and triple, quintuple their salary by going to K Street and lobbying.

AMY GOODMAN: Now, perhaps, with the economy and even these blue chip law firms laying off so many of their associates, maybe there will be a trend in the other direction or at least volunteering at public service law firms and law groups like Legal Services and Legal Aid.

DANIEL BROOK: Well, yes, Amy, we can certainly hope that as these jobs dry out, people will do other things, but I think we need to take a more systematic view of the problem. I mean, just by having these jobs dry up, people with large debt loads are just going to default on their student debt. I think we really need to rethink how we fund higher education in this country, again, and going to the Center for Responsible Lending platform for a 36 percent interest rate cap. Again, I think that would be great, and we should — Senator Durbin has a bill along these lines, that Thomas Geoghegan, who wrote the companion piece in the April issue of Harper’s, mentioned earlier this week on this program — pass that bill.

But what my article tries to do is create a larger context and show why people end up going into the payday lender — things like healthcare reform, where if someone’s child gets sick, it doesn’t put them into the red; something like increased, better public transportation, especially in southern California. If your car breaks down and you’re working poor, you go to the payday lender, and, you know, the public transit is often inadequate to get you to work for a week until you get your car fixed. So we really need to take a much broader look at what kind of country we want to be, if we want to address these problems.

AMY GOODMAN: Daniel Brook, I want to thank you for being with us. He has written his article “Usury Country: Welcome to the Birthplace of Payday Lending” in the latest issue of Harper’s Magazine. His book is called The Trap: Selling Out to Stay Afloat in Winner-Take-All America. And we also want to thank Ginna Green for being with us from California, spokesperson for the Center for Responsible Lending, new report out today on payday loans, and we’ll link to it at democracynow.org.

Media Options